Boosting renewables, better protecting consumers and enhancing industrial competitiveness - these are the three aims the European Commission defined in its proposed reform of the EU electricity market, announced in mid-March. The press release goes into more detail as to how these rather general goals can be achieved, and it’s clear that the flexibility of the power system should play a vital role.

“Member States will now be required to assess their needs, establish objectives to increase non-fossil flexibility, and will have the possibility to introduce new support schemes especially for demand response and storage.”

Industry players welcomed the proposal on demand side flexibility in particular, and the general belief is that, in order to enable this flexibility, smart meters must be deployed across (smart) electricity grids. While they are not the only way to manage demand side flexibility, they are necessary to collect high-resolution data. As behind-the-meter generation, storage, electric vehicle (EV) charging and demand management become more common, grid operators are struggling to keep up. To properly model their networks, they need highly granular data; preferably every 15 or 5 minutes. Smart meters can deliver this data, enabling informed decisions about infrastructure development. But right now, only around 56% of European household consumers have smart meters, and the rollout of these devices across the continent is happening much more slowly than would be desirable. Not only that, there are huge differences between EU member states.

Smart meters on the rise

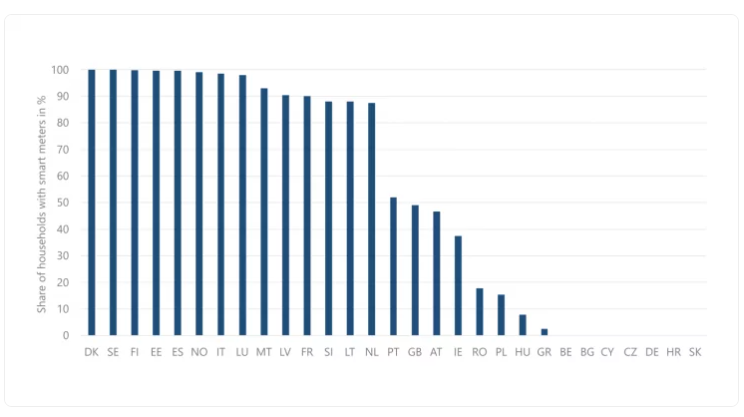

A recent report by research company MarketsandMarkets estimates that the global smart meter market will grow from $23.1 billion to $36.3 billion by 2028, but the performance of individual countries within the EU does not always reflect this explosive growth. Even though around 9.2 million meters were deployed across the continent last year, taking the total number of units to 172 million, when we consider the status of smart meter rollout, we find that some countries have already reached maximum capacity while others are lagging behind. In 2021, the percentage of households equipped with smart meters looked like this:

Scandinavian countries are typically at the forefront of green innovation, so it’s not surprising that they took four of the first six spots. What is striking, however, is that Germany is one of the laggards, with its share absolutely negligible. 0.003%, to be precise: as of 2021, only 160,000 of 50 million metering locations were equipped with smart meters. Considering that Germany is the world’s fourth largest economy and the largest in Europe, these numbers are nothing short of astounding, especially when compared to those of other European countries. Poland, for example, rolled out 360,000 smart meters in the four-year period between 2015 and 2018. Why is it that “progress” has been so slow in Germany?

Smart but complicated

In January, Robert Habeck, Federal Minister for Economic Affairs and Climate Protection, announced a much-needed boost for Germany’s smart meter rollout, acknowledging its importance for the energy transition, promising that “The rollout will be systematized, accelerated and de-bureaucratized.” That pledge gives you an idea why Germany has struggled to date: there has been no clear regulation and the uptake of smart meters has been limited due to legal barriers.

In fairness, taking tens of millions of smart meters into the energy system is a complex project, to say the least. Installation requires significant infrastructure upgrades, which takes time and is expensive. It also involves coordination with multiple stakeholders, such as energy providers, grid operators, meter operators and regulators, which slows down the process. Then there is the question of who is allowed to control these devices, in what circumstances and for whom. Indeed, smart meters do not necessarily have to be controllable. When combined with variable tariffs, one-way meters like the ones widely used in the UK create adequate market incentives for consumers to reduce usage when the price is high. Focusing on these meters would eliminate a lot of the legal complexity that impedes the rollout. But then there is still the financial aspect.

Will consumers have to foot the bill for the installation? Will the amount of energy savings justify the cost of the rollout? Also, will each and every consumer significantly benefit from the technology? There are quite a few uncertainties, but at least the German government answered the first question by saying that the cost for households will be capped at €20 per year. In addition, utilities will be required to offer dynamic price contracts to households with smart meters, starting in 2025. As to the question of who will benefit, innovative energy suppliers may emphasize that it allows their customers to optimize their energy consumption and cut their energy bills, but in the overall scheme of things it’s the planet and, by extension, every single one of us: smart meters reduce the need for fossil fuel-generated electricity, which is beneficial for the environment. Surely everybody, and everything, wins, right?

A rough road, but worth every step

Once again, rolling out smart meters on a large scale is a complex project, and as such the German government’s plan was always going to have both its advocates and its opponents. Even energy companies themselves don’t see eye to eye. E.On, for example, is concerned that the proposal will bring with it its own implementation hurdles, while Octopus Energy supports the plan and would like to see more flexibility from their competitors. Crucially, however, there is an alternative to smart meters.

IoT-enabled devices behind the meter, such as photovoltaic systems, battery storage, heat pumps and EV chargers, can communicate data at the same time granularity as a smart meter. In fact, they go a step beyond smart meters by providing both data and control at the individual device level, giving network operators a much more detailed understanding of each device. This way, they offer a faster path to a large amount of data and device control now, and can later work hand in hand with smart meters to provide a full picture of usage.

Ultimately, then, the smart meter rollout is about much more than just smart meters themselves. They are key to the flexible integration of renewable energy into the power grid but, as noted above, they also bring with them some challenges. Issues like network operators intervening in their consumers’ consumption or decreasing the charging of EVs will remain a bone of contention until clear regulations are introduced.

The ball is now in the court of the Federal Network Agency, and a decision is expected in the fall. The agency already launched a “determination process” last November, its publication on the integration of controllable consumer devices and controllable grid connections providing reassurance that consumers can purchase a heat pump or an EV safe in the knowledge that there will be no waiting time due to congestion in the distribution network.

The government’s goal is to achieve a full rollout of smart meters for residential and small business consumers / generators by 2030. For large users and generators - over 100,000 kWh and over 100 kW, respectively - the date is 2032. Should that target be met, it will provide the infrastructure for a climate-neutral energy system. But we must keep in mind that, even though they have an important role in the future of the country's energy system, smart meters are only part of the solution. Germany is about to smarten up; it now remains to be seen how smart it will actually get.

Related news

-

04-22-24

04-22-24VPP 3.0 - The Third Generation of Virtual Power Plants

-

04-06-24

04-06-24Disaggregation and settlement in virtual power plants

-

03-20-24

03-20-24Dispatching & control of execution in virtual power plants

-

02-08-24

02-08-24How to manage risk for your virtual power plant

-

01-24-24

01-24-24Trading strategies to optimize your virtual power plant